Simanaitis Says

On cars, old, new and future; science & technology; vintage airplanes, computer flight simulation of them; Sherlockiana; our English language; travel; and other stuff

NEW CAR MATH

ARITHMETIC TRENDS of new car purchases are downright scary. According to an item in the Orange County Register, April 21, 2013, auto loans are lengthening to 96 months—that’s eight years! Why anyone would consider such a deal is beyond me.

From the Orange County Register, April 21, 2013.

The article’s headline says, “Pricier cars driving supersizing of loans,” and, indeed, there may be some truth in this. The average transactional price of a new car, according to Kelley Blue Book, is $31,200. However, adjusted for inflation—which is the only sensible way of comparing such data—car prices have risen only modestly over the decades.

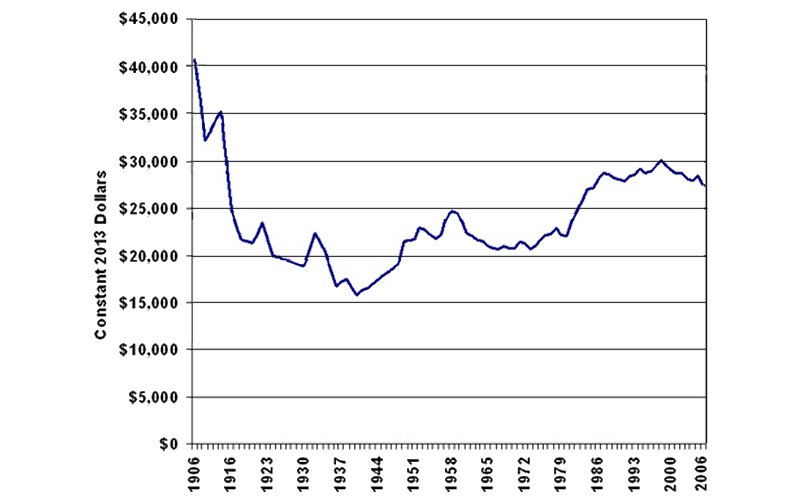

Data from the U.S. Department of Energy (http://goo.gl/TwqZK) give an indication of this. Note: I’ve used the U.S. Department of Labor’s Inflation Calculator (http://goo.gl/WIib) to convert all figures into today’s dollars. For example, the average 2003 new car cost today’s equivalent of $26,780; the average 1993 new car, $27,117 in today’s dollars.

Over the history of the automobile, its inflation-adjusted price dropped significantly, then bounced around but not markedly. Source: U.S. Department of Energy.

Over the really long term—to the birth of the automobile—prices have actually fallen. Working backwards with the Inflation Calculator, the 2013 average new car price of $31,200 translates into $1327 in 1913. To put this figure in perspective, the average automobile—admittedly quite a luxury back then—actually cost its buyer $1431 in those 1913 dollars.

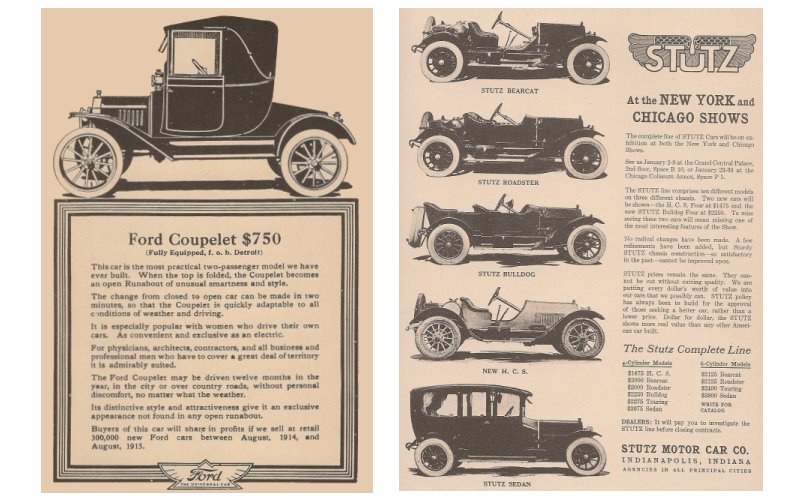

The basic Ford Model T was only $550 in 1913, perhaps a worker’s four months’ pay. No wonder Ford captured 48 percent of the U.S. market by 1914.

There’s an argument that many of today’s buyers should be shopping for the modern equivalent of the 1914 Ford Model T, even if it’s not the car of their dreams (the $2000-$2125 Stutz Bearcat or the luxurious $3675-$3800 Sedan).

But back to today and those scary 96-month auto loans. It used to be that 24- and 36-month deals were the standard. However, according to J.D. Power and Associates, nearly one-third of today’s loans are for 72 months or longer.

True, interest rates generally are at historic lows, but extended loans pay interest for longer times and typically are accompanied by higher rates. This in turn means that, for a longer period of time, extended-loan buyers remain “upside-down,” their cars worth less than the money owed. A typical buyer could be underwater for five of the seven years of such a loan.

It’s true that the average age of today’s fleet is 11 years. But does it make sense to have negative equity for more than two-thirds of this time?

A more rational approach is to use the 20-4-10 rule. Put 20 percent down on the new car purchase. Borrow for no more than four years/48-months. And keep monthly payments within 10 percent of gross monthly income. Car enthusiasts may stretch this to 20 percent of monthly take-home.

Alas, not many people are listening. According to Experian Automotive, 89 percent of buyers are breaking the four-year rule.

Maybe it’s a good time to invest in the repo business? ds

© Dennis Simanaitis, SimanaitisSays.com, 2013